Table of Contents

- Introduction

- Understanding Business Lines of Credit

- Types of Business Lines of Credit

- Factors to Consider When Choosing a Line of Credit

- Conclusion

Introduction

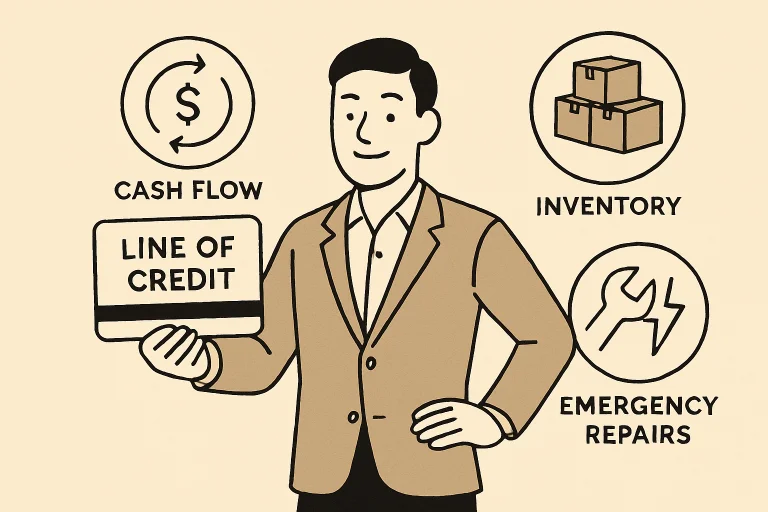

Entrepreneurs often face challenges that demand quick, reliable funding, whether to improve cash flow, fund new projects, or address unforeseen expenses. The nature of running a business can be unpredictable, frequently requiring access to capital at short notice whether to purchase inventory, cover payroll, or address emergency repairs. Among the numerous financing options available, securing the best business line of credit can be a game-changer, offering crucial flexibility to draw and repay funds as needed. This solution ensures businesses pay interest only on what they use providing a practical and affordable lifeline for growth and stability. Business lines of credit are instrumental because they provide a financial safety net that can help maintain steady operations through both regular ebb and flow and sudden market changes.

With today’s fast-paced business landscape, leveraging a business line of credit has become increasingly common among startups and established firms alike. Many entrepreneurs recognize that having pre-approved access to capital can mean the difference between seizing a growth opportunity and missing it due to a lack of funds. Understanding the nuances, eligibility requirements, and standout lenders in this space is essential for making informed financial decisions that will set your company up for long-term success. It’s important for business owners not only to know what options are available but also to recognize how each financial product fits into their specific strategy for stability and expansion.

Understanding Business Lines of Credit

A business line of credit is fundamentally different from other forms of business financing, such as term loans or merchant cash advances. It operates as a revolving account that offers entrepreneurs a maximum draw limit, allowing them to borrow, repay, and borrow again within that limit. Unlike a traditional business loan, which provides a lump-sum of cash with a fixed repayment schedule, a line of credit functions much like a credit card for your business, allowing you to access funds as needed up to the approved limit. According to Investopedia, a business line of credit allows companies to “borrow, repay, and borrow again” within a set limit, making it a flexible option for managing cash flow gaps. This revolving feature makes it ideal for addressing working capital needs, handling seasonal fluctuations, or managing payroll during slow periods, without locking you into a rigid repayment plan for a single disbursement.

Because a line of credit is not a one-time lump sum, it offers control over how much to borrow and when, giving owners the agility to fund operations or seize sudden opportunities. Some businesses use their lines of credit to bridge gaps when client payments are delayed, while others draw on funds to smooth out off-peak or slow sales cycles. These features make business lines of credit a top choice for businesses aiming for both flexibility and financial control. By utilizing this financing tool, entrepreneurs can respond more confidently to new possibilities or challenges, protecting the company’s overall financial health and improving long-term prospects.

Types of Business Lines of Credit

- Secured Line of Credit: This type requires collateral, such as business assets or inventory, and typically results in more favorable interest rates due to the reduced risk for lenders. Collateral can range from equipment to real estate, and providing it often opens doors to higher credit limits and longer repayment terms.

- Unsecured Line of Credit: Lenders do not require collateral but often set higher interest rates and stricter criteria, making these lines more accessible to well-established businesses with excellent credit profiles. Businesses that qualify for unsecured lines typically demonstrate solid income, a strong business history, and positive credit performance, providing lenders with peace of mind despite the lack of assets securing the funds.

- Revolving Line of Credit: As payments are made, available credit is restored, allowing continual access to funds. It is ideal for ongoing or unpredictable expenses, such as covering cyclical cash flow gaps, funding recurring projects, or preparing for unforeseen market shifts. This option is especially appealing to businesses that need a flexible, reusable source of funding.

- Non-Revolving Line of Credit: This line provides a single draw up to a fixed amount; once repaid, it cannot be borrowed again. It’s suitable for one-off or planned expenses, such as a specific expansion project or a large equipment purchase where ongoing access to funds isn’t necessary. The non-revolving nature can also help businesses budget more precisely, as they know exactly how much they can use and when repayment will be complete.

Factors to Consider When Choosing a Line of Credit

- Interest Rates: Always compare the annual percentage rate (APR) from several lenders to find an option that keeps long-term costs manageable. Remember that a lower APR can make a significant difference in your repayments, especially if you plan to draw on your credit line intermittently or over a long period.

- Credit Limits: Consider how the upper borrowing limit aligns with your expected financing needs too little, and it won’t help; too much, and it might lead to costly borrowing temptations. It’s best to estimate your cash flow cycles and identify months when extra funding is most necessary, ensuring your line of credit matches actual needs without encouraging wasteful spending.

- Repayment Terms: Understand your repayment schedule, draw and inactivity fees, and any penalties for early payoff. Clarity here prevents surprises. Some lines of credit also feature maintenance fees or minimum usage charges, so it’s crucial to read the fine print before committing. Make sure you understand how regularly you need to make payments, and what happens if you exceed your limit or pay off your balance early.

- Eligibility Requirements: Check your business’s operating history, revenue thresholds, and credit score before starting the application process to avoid wasted time or unnecessary credit inquiries. Lenders may pull your personal and business credit during the application, so being prepared with financial statements and understanding their criteria can speed up the process and increase your chances of approval.

Conclusion

Evaluating and selecting the right business line of credit is a significant step for any entrepreneur looking to enhance operational agility and safeguard business growth. Choosing the correct option involves more than comparing interest rates—it’s about finding a lender with criteria, terms, and features that align with your current finances and strategic direction. Comparing top lenders, understanding the distinct types of credit lines, and reviewing terms and eligibility will ensure you secure the financing solution that matches your business’s evolving demands. The right line of credit gives your company the power to survive difficult periods, invest in expansion, and keep operations running smoothly when cash flow becomes tight.